Every mortgage lender has a story about the opportunity that got away. Maybe it was missing a demographic shift in your market, or failing to spot a competitor's pricing strategy until it was too late. Perhaps you watched a smaller lender capture market share by serving a borrower segment you didn't even know existed.

The mortgage industry is full of these stories, and they all have something in common: the data was there, but the systematic approach to analyze it wasn't. While your competitors are still making decisions based on gut instinct, the most successful lenders are building innovation strategies around comprehensive data analysis.

But mortgage banking faces a unique innovation challenge that makes systematic approaches even more critical: we're operating in one of the most heavily regulated industries in the U.S. Unlike tech companies that can "move fast and break things," mortgage lenders must innovate within strict compliance frameworks. OCC, FDIC, NCUA, HUD regulations, CFPB enforcement actions, fair lending scrutiny, and HMDA reporting requirements mean that every strategic decision carries regulatory risk.

This regulatory reality doesn't constrain innovation - it demands more sophisticated innovation. When you can't afford to make mistakes, you need data-driven validation before implementing new strategies. When fair lending compliance requires demonstrable non-discrimination, you need transparent data sources that can withstand regulatory examination. When CFPB enforcement increasingly focuses on "black box" decision-making systems, you need clear data lineage for every business choice.

The question isn't whether growth opportunities exist in today's challenging market - they do. In 2024, the mortgage market grew more than 8% year-over-year to 6.2 Million loans, despite the persistent high interest rates and housing affordability. The question is whether you have the systematic approach to find these growth opportunities to, validate them, and act on them before your competition does. Thirteen out of the top fifty mortgage lenders diverged from the growth trajectory and experienced a decline in a growing market.

Here's the uncomfortable truth about mortgage banking innovation: most of it fails not because of bad ideas, but because of bad information. Lenders launch new products based on assumptions or enter new markets based on hunches only to face fair lending challenges, CFPB scrutiny, or compliance violations they never anticipated.

The regulatory environment fundamentally changes the innovation game. Unlike less regulated industries where you can test, fail, and iterate quickly, mortgage banking requires extensive upfront validation. Every demographic targeting strategy must be defensible under fair lending laws. Every pricing innovation must withstand CFPB examination. Every market expansion must demonstrate compliance with local and federal regulations.

You might be thinking - innovation in mortgage banking is impossible. But the regulatory reality of our industry just means that you need a systematic, data-driven innovation. When regulators increasingly focus on algorithmic bias and "black box" decision-making, transparent data sources become competitive advantages. When fair lending compliance requires demonstrable non-discrimination, comprehensive demographic analysis becomes business necessity, not just market intelligence.

The successful lenders, the ones growing market share even in tough conditions, have flipped this approach. They start with regulatory-grade data analysis, identify opportunities that can withstand compliance scrutiny, then build targeted strategies around empirical evidence that regulators will respect.

This systematic approach to innovation isn't new. Management expert Peter Drucker identified seven sources of innovation opportunity decades ago, but his framework becomes exponentially more powerful when combined with today's mortgage data capabilities. The sources of innovation are in the unexpected occurrences, incongruities, process needs, industry and market changes, demographic changes, changes in perception, and new knowledge.

Instead of waiting for genius to strike, you can methodically analyze where your next growth opportunities are hiding.

The most reliable innovation opportunities come from demographic changes, precisely because they have known lead times. Every person who will be in the homebuying market over the next decade is already identifiable in today's data. The challenge is knowing where to look and how to interpret what you're seeing.

Start with first-time homebuyers, but go deeper than the conventional wisdom that they're all priced out. When you analyze loan-level data through comprehensive platforms, a more nuanced picture emerges. Yes, traditional first-time buyer activity is down, but certain segments are actually increasing their participation.

The delayed homebuyer phenomenon represents a concrete opportunity most lenders are missing. Professionals who traditionally would have bought homes in their late twenties are now entering the market in their mid-thirties. They are a fundamentally different customer segment with higher incomes, larger down payments, and distinct preferences around loan products and digital experience.

Here's how to identify these patterns in your market data: Look for application volume trends by age cohort, income brackets, and employment type. Compare current patterns to historical norms over two to seven-year periods. Pay particular attention to segments where volume is increasing even as overall market activity declines.

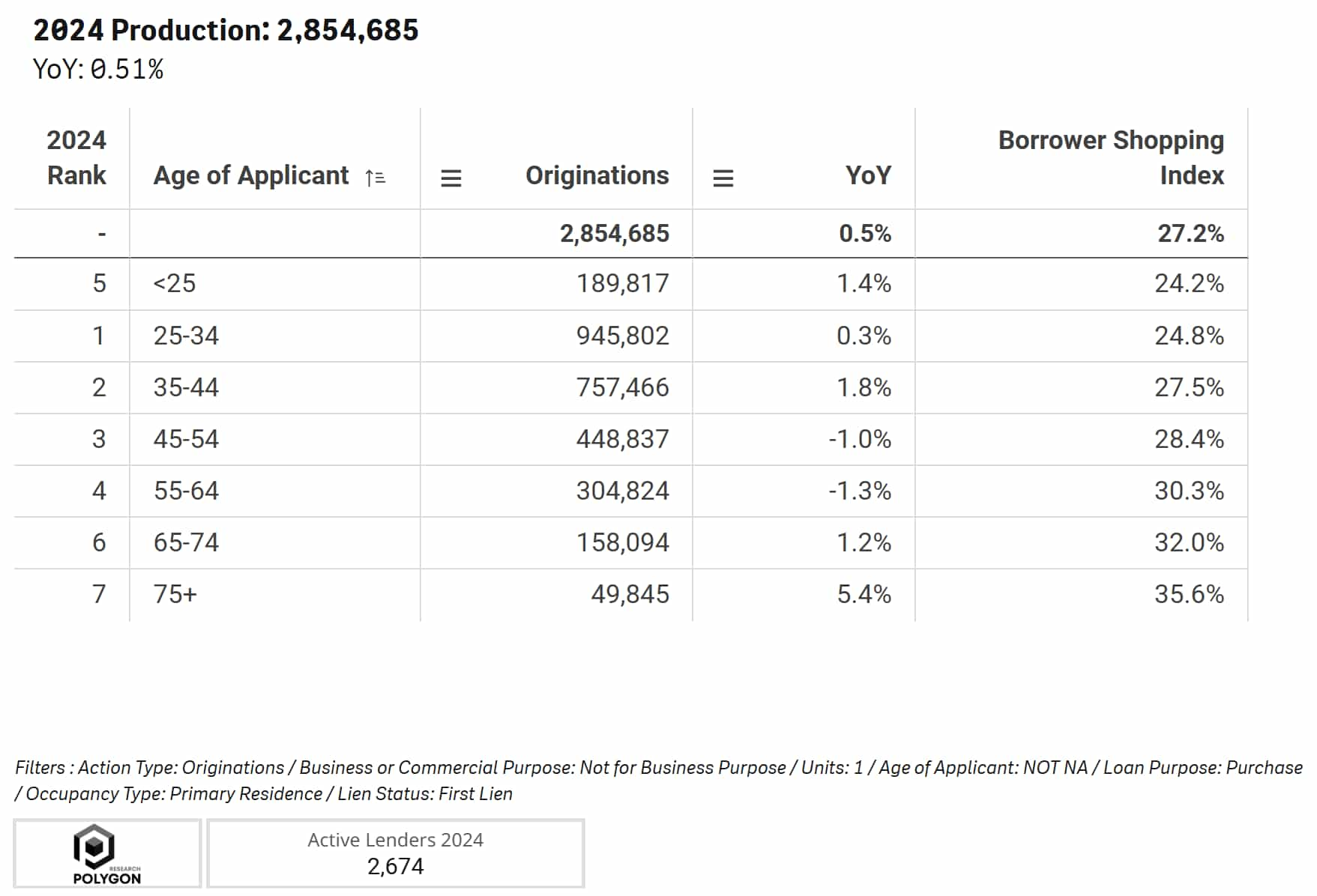

Here is one example of analysis by Age of Borrower - loan production, Y-o-Y growth, and Borrower Shopping Index.

Geographic redistribution creates another systematic opportunity. Remote work changed where people live relative to where they work. This also changed how people shop for mortgages and what they need from lenders. Borrowers are increasingly disconnected from their local markets, creating gaps that data-savvy lenders can fill with superior market intelligence and education.

To spot these geographic opportunities, analyze origination patterns by metropolitan area, looking for markets with increasing purchase activity from out-of-state borrowers. Cross-reference this with employment data to identify which industries are driving the migration. Then examine the competitive landscape in these markets to find underserved segments. These insights are easily discoverable through American Community Survey (ACS) data, which we model for instant analysis in CensusVision. We use the 1 Year microdata (PUMS) in order to help you discover those changes and spot those patterns.

The key insight is precision. Instead of broad demographic generalizations, use loan-level analysis and microdata from the ACS to identify specific borrower profiles, specific geographic markets, and specific product preferences that create actionable opportunities.

While demographic changes provide reliable long-term opportunities, market disruptions create immediate innovation possibilities for lenders who can recognize and respond quickly. The current high-rate environment exemplifies this perfectly.

Most mortgage lenders see elevated rates as purely constraining, a problem to survive rather than an opportunity to exploit. But market disruptions typically create winners and losers, and the winners are usually those who adapt their strategies to new realities rather than waiting for old conditions to return.

High rates have fundamentally altered the competitive landscape beyond just reducing volume. Traditional product differentiation has narrowed as rate sensitivity dominates borrower decisions, but this constraint has simultaneously created new opportunities for specialized positioning.

The refinance market's transformation illustrates this opportunity. Traditional rate-and-term refinances have largely disappeared, but cash-out refinances for home improvements, debt consolidation, and investment purposes remain active among specific borrower segments. The innovation lies in identifying which segments, in which markets, and with what specific needs are still actively refinancing.

Here's your systematic approach: Use monthly origination data to track refinance activity by loan type, key borrower characteristics like credit score and DTI ratios, first-time buyer status, and geographic markets. Look for pockets of sustained activity even as overall refinance volume declines. Then analyze the competitive landscape in these niches to identify positioning opportunities.

Consider this real-world example from 2025 California cash-out refinance activity, broken down by credit score and CLTV ranges.

While most lenders focus on the 780+ credit score borrowers, systematic analysis reveals substantial volume in the 740-780 range with moderate CLTV ratios, a segment that's both profitable and often underserved. And at the very least, by understanding the playing field, you can use the data insight to help you position your organization to capture the opportunity and to win.

The purchase market has stratified in ways that weren't apparent during ultra-low rate environments. High-end purchases continue with different financing patterns, investor activity has shifted to new geographies and property types, and certain first-time buyer segments lean into government products.

To identify these opportunities, examine origination trends by loan amount, property type, and borrower characteristics. Compare current market share distributions to historical patterns. Pay attention to segments where your competitors have reduced focus, creating openings for specialized products or services.

The systematic advantage comes from understanding exactly how market changes affect different borrower types, product categories, and geographic markets. While most lenders retreat to familiar strategies, innovation opportunities exist in serving the emerging needs that others are overlooking.

Before you can build a systematic innovation approach in mortgage banking, you need to address a fundamental question that doesn't apply in less regulated industries: where is your data coming from, and can you defend it to regulators?

This isn't just a technical issue or a question asked by nerds - it's a legal and strategic imperative. The mortgage industry is flooded with demographic and market data products, but many lack the transparency and verifiable lineage that serious business decisions require. Smart lenders build innovation strategies assuming future regulatory scrutiny, because enforcement priorities can shift quickly. When facing potential CFPB examination, fair lending audits, or regulatory challenges, you can't afford to base decisions on data of questionable origin or methodology.

The gold standard for demographic and mortgage analysis remains open government data sources: HMDA (Home Mortgage Disclosure Act), Census Bureau datasets including the American Community Survey (ACS), Current Population Survey (CPS), and Annual Social and Economic Supplement (ASEC). These sources provide complete transparency about methodology, collection processes, and data lineage, exactly what regulators expect when examining your decision-making processes.

Here's why this matters for innovation in mortgage banking: when you identify an opportunity in open data, you can trace exactly where that insight comes from, validate it independently, and defend your strategic response to any regulatory inquiry. When demographic patterns emerge from HMDA loan-level data combined with Census demographic profiles, you're seeing real market behavior documented in public records, not modeled estimates or proprietary algorithms that you can't explain to examiners.

Any other dataset that claims to provide demographic and mortgage insights should face rigorous questioning: How was this data collected? What's the methodology? Can you verify the sources? Is there potential bias in collection or processing? Most importantly, can you replicate the analysis independently and explain it to regulators?

Can you replicate the analysis independently and explain it to regulators?

The innovation advantage in mortgage banking comes not just from having data, but from having defensible data with clear provenance. When you're making strategic bets that could face regulatory scrutiny, transparency is essential for sustainable growth.

The most successful mortgage lenders don't stumble onto opportunities—they systematically discover them through interactive dashboards that function as innovation command centers. While many vendors offer what they call "market intelligence" - filterable, but yet simple lists of loan officers, real estate agents, and borrowers' names and addresses - the strategic question becomes: what good will contact lists do in an era where Rocket Mortgage acquired Redfin, consolidation reshapes entire markets, and AI transforms customer acquisition?

Today's innovation requires a three-dimensional view of mortgage market reality. You need platforms like Polygon Vision and Polygon Pulse that allow you to think strategically, not just appear to be analyzing data. These aren't reporting tools - they're interactive environments where you can ask and answer complex questions about demographic shifts, competitive positioning, and market structure changes in real-time.

Your innovation strategy starts with comprehensive data integration across loan-level originations, demographic analysis connecting borrower characteristics to market trends, and competitive intelligence revealing structural market changes. For that, you need the analytical capability to examine these data sources simultaneously, identifying patterns that create competitive advantages before they become obvious to everyone else.

This approach validates and amplifies your market instincts rather than replacing them. The best executives combine market intuition with empirical evidence, using interactive dashboards to test hypotheses, validate opportunities, and build confidence in strategic decisions. When you can drill down from market-level trends to borrower-specific patterns instantly, you're operating with fundamentally different capabilities than competitors relying on static reports.

Focus on leading indicators through monthly analysis cycles that reveal emerging opportunities before they appear in quarterly industry publications. Instead of monitoring overall trends, examine segment-specific patterns revealing opportunities within broader market movements.

Your competitive advantage comes from seeing patterns earlier and acting faster than competitors using conventional market intelligence. When you have systematic visibility into demographic shifts, market changes, and competitive gaps through sophisticated analytical platforms, innovation becomes a disciplined capability rather than an occasional accident.

The mortgage bankers who will lead the next wave of industry growth won't be waiting for market conditions to improve or hoping for genius insights to strike. They'll be systematically analyzing comprehensive data, identifying specific opportunities, and building targeted strategies around empirical evidence.

Consider this real example: While most lenders assumed young borrowers were completely priced out of the market, our analysis revealed that borrowers under 35 actually represent specific geographic and product opportunities worth millions in potential originations. The key was knowing where to look and how to analyze the patterns.

This systematic approach transforms innovation from a luxury you pursue when times are good into a competitive necessity that drives growth even in challenging conditions. When you can identify demographic opportunities before they become obvious, capitalize on market disruptions while others retreat, and build systematic processes for ongoing opportunity identification, you're operating with fundamentally different capabilities than competitors relying on intuition alone.

The data exists to support this systematic approach. Comprehensive loan-level databases, demographic analysis platforms, and competitive intelligence tools provide the raw material for identifying innovation opportunities. The question is whether you'll develop the systematic capability to analyze this information, validate opportunities, and act on insights faster than competitors still making decisions based on gut instinct and quarterly reports.

See this systematic approach in action. Watch our 2-minute analysis, where we walk through the exact process of identifying opportunities among borrowers under 35 (the same demographic most lenders have written off as a segment that is priced out of the market). You'll see how we use HMDAVision (bundled with CensusVision in Polygon Vision suite) to uncover patterns that create actionable business strategies.

In an industry where traditional playbooks are being rewritten, systematic innovation is becoming a survival requirement. The lenders who thrive will be those who master the discipline of turning data into actionable opportunities before their competition even knows those opportunities exist.

Ready to dive deeper into demographic opportunities? Download our complete Under-35 Borrower Analysis Report for the full demographic breakdown, geographic patterns, and market opportunities that complement the methodology shown in our video analysis.

Learn how mortgage lenders use data to identify growth opportunities, spot demographic shifts, and capitalize on market changes before competitors.

Every mortgage lender has a story about the opportunity that got away. Maybe it was missing a demographic shift in your market, or failing to spot a competitor's pricing strategy until it was too late. Perhaps you watched a smaller lender capture market share by serving a borrower segment you didn't even know existed.

The mortgage industry is full of these stories, and they all have something in common: the data was there, but the systematic approach to analyze it wasn't. While your competitors are still making decisions based on gut instinct, the most successful lenders are building innovation strategies around comprehensive data analysis.

But mortgage banking faces a unique innovation challenge that makes systematic approaches even more critical: we're operating in one of the most heavily regulated industries in the U.S. Unlike tech companies that can "move fast and break things," mortgage lenders must innovate within strict compliance frameworks. OCC, FDIC, NCUA, HUD regulations, CFPB enforcement actions, fair lending scrutiny, and HMDA reporting requirements mean that every strategic decision carries regulatory risk.

This regulatory reality doesn't constrain innovation - it demands more sophisticated innovation. When you can't afford to make mistakes, you need data-driven validation before implementing new strategies. When fair lending compliance requires demonstrable non-discrimination, you need transparent data sources that can withstand regulatory examination. When CFPB enforcement increasingly focuses on "black box" decision-making systems, you need clear data lineage for every business choice.

The question isn't whether growth opportunities exist in today's challenging market - they do. In 2024, the mortgage market grew more than 8% year-over-year to 6.2 Million loans, despite the persistent high interest rates and housing affordability. The question is whether you have the systematic approach to find these growth opportunities to, validate them, and act on them before your competition does. Thirteen out of the top fifty mortgage lenders diverged from the growth trajectory and experienced a decline in a growing market.

Here's the uncomfortable truth about mortgage banking innovation: most of it fails not because of bad ideas, but because of bad information. Lenders launch new products based on assumptions or enter new markets based on hunches only to face fair lending challenges, CFPB scrutiny, or compliance violations they never anticipated.

The regulatory environment fundamentally changes the innovation game. Unlike less regulated industries where you can test, fail, and iterate quickly, mortgage banking requires extensive upfront validation. Every demographic targeting strategy must be defensible under fair lending laws. Every pricing innovation must withstand CFPB examination. Every market expansion must demonstrate compliance with local and federal regulations.

You might be thinking - innovation in mortgage banking is impossible. But the regulatory reality of our industry just means that you need a systematic, data-driven innovation. When regulators increasingly focus on algorithmic bias and "black box" decision-making, transparent data sources become competitive advantages. When fair lending compliance requires demonstrable non-discrimination, comprehensive demographic analysis becomes business necessity, not just market intelligence.

The successful lenders, the ones growing market share even in tough conditions, have flipped this approach. They start with regulatory-grade data analysis, identify opportunities that can withstand compliance scrutiny, then build targeted strategies around empirical evidence that regulators will respect.

This systematic approach to innovation isn't new. Management expert Peter Drucker identified seven sources of innovation opportunity decades ago, but his framework becomes exponentially more powerful when combined with today's mortgage data capabilities. The sources of innovation are in the unexpected occurrences, incongruities, process needs, industry and market changes, demographic changes, changes in perception, and new knowledge.

Instead of waiting for genius to strike, you can methodically analyze where your next growth opportunities are hiding.

The most reliable innovation opportunities come from demographic changes, precisely because they have known lead times. Every person who will be in the homebuying market over the next decade is already identifiable in today's data. The challenge is knowing where to look and how to interpret what you're seeing.

Start with first-time homebuyers, but go deeper than the conventional wisdom that they're all priced out. When you analyze loan-level data through comprehensive platforms, a more nuanced picture emerges. Yes, traditional first-time buyer activity is down, but certain segments are actually increasing their participation.

The delayed homebuyer phenomenon represents a concrete opportunity most lenders are missing. Professionals who traditionally would have bought homes in their late twenties are now entering the market in their mid-thirties. They are a fundamentally different customer segment with higher incomes, larger down payments, and distinct preferences around loan products and digital experience.

Here's how to identify these patterns in your market data: Look for application volume trends by age cohort, income brackets, and employment type. Compare current patterns to historical norms over two to seven-year periods. Pay particular attention to segments where volume is increasing even as overall market activity declines.

Here is one example of analysis by Age of Borrower - loan production, Y-o-Y growth, and Borrower Shopping Index.

Geographic redistribution creates another systematic opportunity. Remote work changed where people live relative to where they work. This also changed how people shop for mortgages and what they need from lenders. Borrowers are increasingly disconnected from their local markets, creating gaps that data-savvy lenders can fill with superior market intelligence and education.

To spot these geographic opportunities, analyze origination patterns by metropolitan area, looking for markets with increasing purchase activity from out-of-state borrowers. Cross-reference this with employment data to identify which industries are driving the migration. Then examine the competitive landscape in these markets to find underserved segments. These insights are easily discoverable through American Community Survey (ACS) data, which we model for instant analysis in CensusVision. We use the 1 Year microdata (PUMS) in order to help you discover those changes and spot those patterns.

The key insight is precision. Instead of broad demographic generalizations, use loan-level analysis and microdata from the ACS to identify specific borrower profiles, specific geographic markets, and specific product preferences that create actionable opportunities.

While demographic changes provide reliable long-term opportunities, market disruptions create immediate innovation possibilities for lenders who can recognize and respond quickly. The current high-rate environment exemplifies this perfectly.

Most mortgage lenders see elevated rates as purely constraining, a problem to survive rather than an opportunity to exploit. But market disruptions typically create winners and losers, and the winners are usually those who adapt their strategies to new realities rather than waiting for old conditions to return.

High rates have fundamentally altered the competitive landscape beyond just reducing volume. Traditional product differentiation has narrowed as rate sensitivity dominates borrower decisions, but this constraint has simultaneously created new opportunities for specialized positioning.

The refinance market's transformation illustrates this opportunity. Traditional rate-and-term refinances have largely disappeared, but cash-out refinances for home improvements, debt consolidation, and investment purposes remain active among specific borrower segments. The innovation lies in identifying which segments, in which markets, and with what specific needs are still actively refinancing.

Here's your systematic approach: Use monthly origination data to track refinance activity by loan type, key borrower characteristics like credit score and DTI ratios, first-time buyer status, and geographic markets. Look for pockets of sustained activity even as overall refinance volume declines. Then analyze the competitive landscape in these niches to identify positioning opportunities.

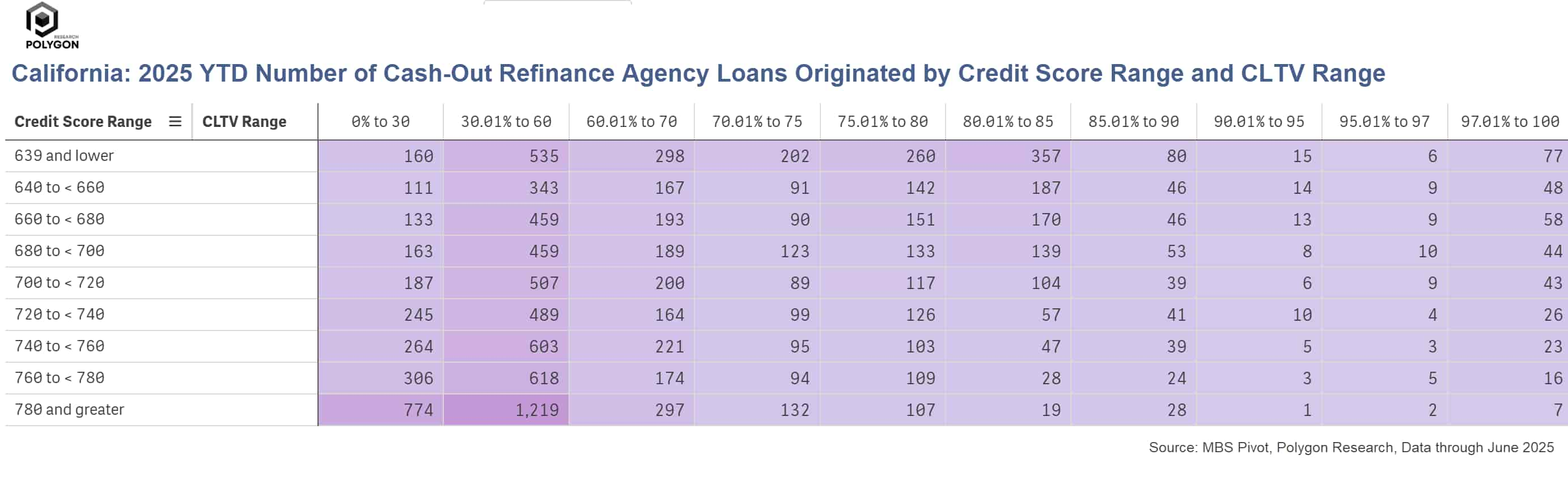

Consider this real-world example from 2025 California cash-out refinance activity, broken down by credit score and CLTV ranges.

While most lenders focus on the 780+ credit score borrowers, systematic analysis reveals substantial volume in the 740-780 range with moderate CLTV ratios, a segment that's both profitable and often underserved. And at the very least, by understanding the playing field, you can use the data insight to help you position your organization to capture the opportunity and to win.

The purchase market has stratified in ways that weren't apparent during ultra-low rate environments. High-end purchases continue with different financing patterns, investor activity has shifted to new geographies and property types, and certain first-time buyer segments lean into government products.

To identify these opportunities, examine origination trends by loan amount, property type, and borrower characteristics. Compare current market share distributions to historical patterns. Pay attention to segments where your competitors have reduced focus, creating openings for specialized products or services.

The systematic advantage comes from understanding exactly how market changes affect different borrower types, product categories, and geographic markets. While most lenders retreat to familiar strategies, innovation opportunities exist in serving the emerging needs that others are overlooking.

Before you can build a systematic innovation approach in mortgage banking, you need to address a fundamental question that doesn't apply in less regulated industries: where is your data coming from, and can you defend it to regulators?

This isn't just a technical issue or a question asked by nerds - it's a legal and strategic imperative. The mortgage industry is flooded with demographic and market data products, but many lack the transparency and verifiable lineage that serious business decisions require. Smart lenders build innovation strategies assuming future regulatory scrutiny, because enforcement priorities can shift quickly. When facing potential CFPB examination, fair lending audits, or regulatory challenges, you can't afford to base decisions on data of questionable origin or methodology.

The gold standard for demographic and mortgage analysis remains open government data sources: HMDA (Home Mortgage Disclosure Act), Census Bureau datasets including the American Community Survey (ACS), Current Population Survey (CPS), and Annual Social and Economic Supplement (ASEC). These sources provide complete transparency about methodology, collection processes, and data lineage, exactly what regulators expect when examining your decision-making processes.

Here's why this matters for innovation in mortgage banking: when you identify an opportunity in open data, you can trace exactly where that insight comes from, validate it independently, and defend your strategic response to any regulatory inquiry. When demographic patterns emerge from HMDA loan-level data combined with Census demographic profiles, you're seeing real market behavior documented in public records, not modeled estimates or proprietary algorithms that you can't explain to examiners.

Any other dataset that claims to provide demographic and mortgage insights should face rigorous questioning: How was this data collected? What's the methodology? Can you verify the sources? Is there potential bias in collection or processing? Most importantly, can you replicate the analysis independently and explain it to regulators?

Can you replicate the analysis independently and explain it to regulators?

The innovation advantage in mortgage banking comes not just from having data, but from having defensible data with clear provenance. When you're making strategic bets that could face regulatory scrutiny, transparency is essential for sustainable growth.

The most successful mortgage lenders don't stumble onto opportunities—they systematically discover them through interactive dashboards that function as innovation command centers. While many vendors offer what they call "market intelligence" - filterable, but yet simple lists of loan officers, real estate agents, and borrowers' names and addresses - the strategic question becomes: what good will contact lists do in an era where Rocket Mortgage acquired Redfin, consolidation reshapes entire markets, and AI transforms customer acquisition?

Today's innovation requires a three-dimensional view of mortgage market reality. You need platforms like Polygon Vision and Polygon Pulse that allow you to think strategically, not just appear to be analyzing data. These aren't reporting tools - they're interactive environments where you can ask and answer complex questions about demographic shifts, competitive positioning, and market structure changes in real-time.

Your innovation strategy starts with comprehensive data integration across loan-level originations, demographic analysis connecting borrower characteristics to market trends, and competitive intelligence revealing structural market changes. For that, you need the analytical capability to examine these data sources simultaneously, identifying patterns that create competitive advantages before they become obvious to everyone else.

This approach validates and amplifies your market instincts rather than replacing them. The best executives combine market intuition with empirical evidence, using interactive dashboards to test hypotheses, validate opportunities, and build confidence in strategic decisions. When you can drill down from market-level trends to borrower-specific patterns instantly, you're operating with fundamentally different capabilities than competitors relying on static reports.

Focus on leading indicators through monthly analysis cycles that reveal emerging opportunities before they appear in quarterly industry publications. Instead of monitoring overall trends, examine segment-specific patterns revealing opportunities within broader market movements.

Your competitive advantage comes from seeing patterns earlier and acting faster than competitors using conventional market intelligence. When you have systematic visibility into demographic shifts, market changes, and competitive gaps through sophisticated analytical platforms, innovation becomes a disciplined capability rather than an occasional accident.

The mortgage bankers who will lead the next wave of industry growth won't be waiting for market conditions to improve or hoping for genius insights to strike. They'll be systematically analyzing comprehensive data, identifying specific opportunities, and building targeted strategies around empirical evidence.

Consider this real example: While most lenders assumed young borrowers were completely priced out of the market, our analysis revealed that borrowers under 35 actually represent specific geographic and product opportunities worth millions in potential originations. The key was knowing where to look and how to analyze the patterns.

This systematic approach transforms innovation from a luxury you pursue when times are good into a competitive necessity that drives growth even in challenging conditions. When you can identify demographic opportunities before they become obvious, capitalize on market disruptions while others retreat, and build systematic processes for ongoing opportunity identification, you're operating with fundamentally different capabilities than competitors relying on intuition alone.

The data exists to support this systematic approach. Comprehensive loan-level databases, demographic analysis platforms, and competitive intelligence tools provide the raw material for identifying innovation opportunities. The question is whether you'll develop the systematic capability to analyze this information, validate opportunities, and act on insights faster than competitors still making decisions based on gut instinct and quarterly reports.

See this systematic approach in action. Watch our 2-minute analysis, where we walk through the exact process of identifying opportunities among borrowers under 35 (the same demographic most lenders have written off as a segment that is priced out of the market). You'll see how we use HMDAVision (bundled with CensusVision in Polygon Vision suite) to uncover patterns that create actionable business strategies.

In an industry where traditional playbooks are being rewritten, systematic innovation is becoming a survival requirement. The lenders who thrive will be those who master the discipline of turning data into actionable opportunities before their competition even knows those opportunities exist.

Ready to dive deeper into demographic opportunities? Download our complete Under-35 Borrower Analysis Report for the full demographic breakdown, geographic patterns, and market opportunities that complement the methodology shown in our video analysis.