Agency Rate-Term Refi Average LTV by State: TTM January 2026

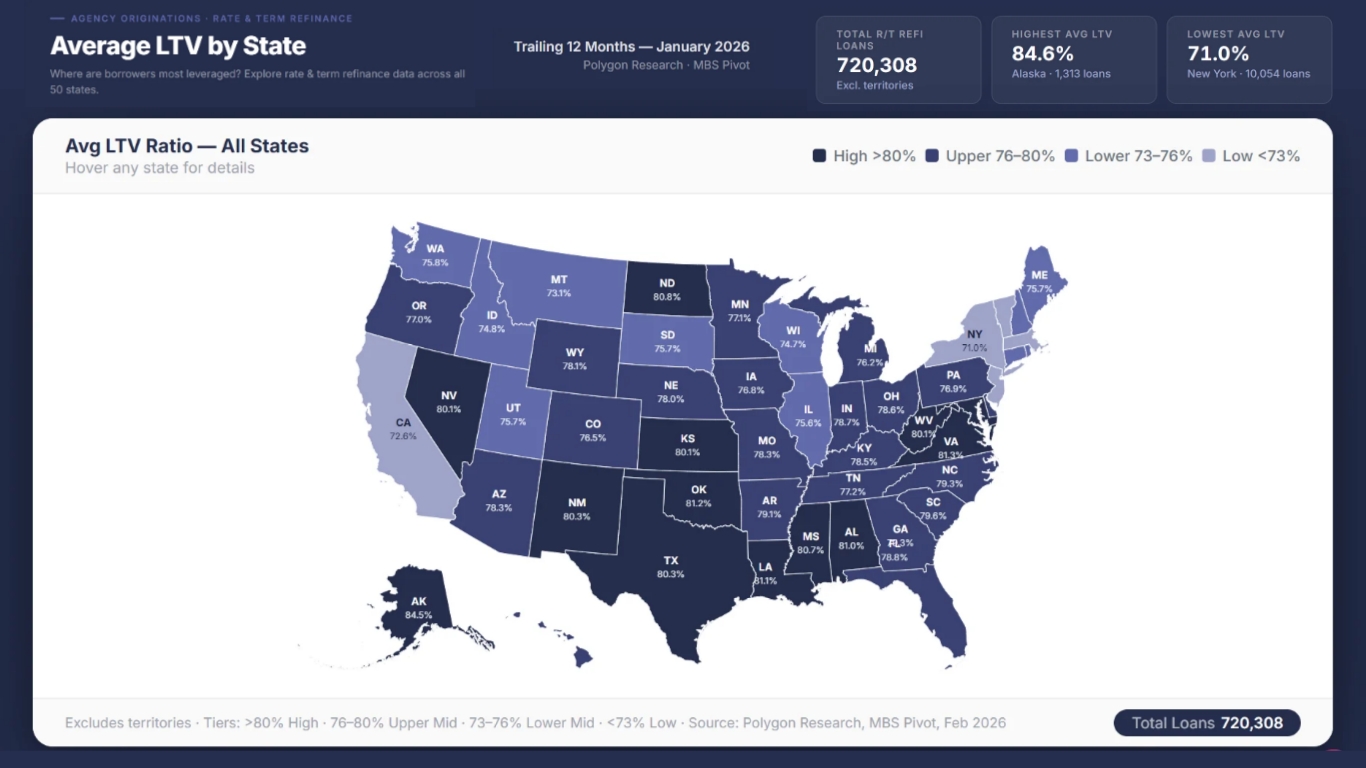

This map presents trailing 12-month (TTM) average LTV for agency rate-and-term refinances through January 2026 . Several states exceed 80% average LTV—including Alaska (84.5%), Virginia (81.3%), Oklahoma (81.2%), and Louisiana (81.1%)—indicating thinner borrower equity cushions in recent refi activity. In contrast, large production states such as California (72.6%), Florida (78.8%), and Texas (80.3%) show more moderate profiles relative to some smaller markets.

For lenders, this dispersion matters operationally and financially. Higher average LTV increases exposure to collateral volatility, MI reliance, and potential repurchase sensitivity, particularly if home price appreciation moderates. Secondary marketing teams should assess whether geographic concentration at elevated LTVs is aligned with hedge coverage, SRP execution, and capital allocation. Servicing leaders should also evaluate prepayment and default sensitivity in high-LTV cohorts, as thinner equity can amplify both refi incentives (if rates fall) and credit stress (if prices soften).

Strategically, this data supports tighter appraisal QC in high-LTV geographies and enhanced monitoring of state-level house price trends.

From Analysis to Action

Ready to Continue? Get Your Exact Market Answers.

Start your 7-day free trial.