DC Zipcode Refinance Incentive Ratios

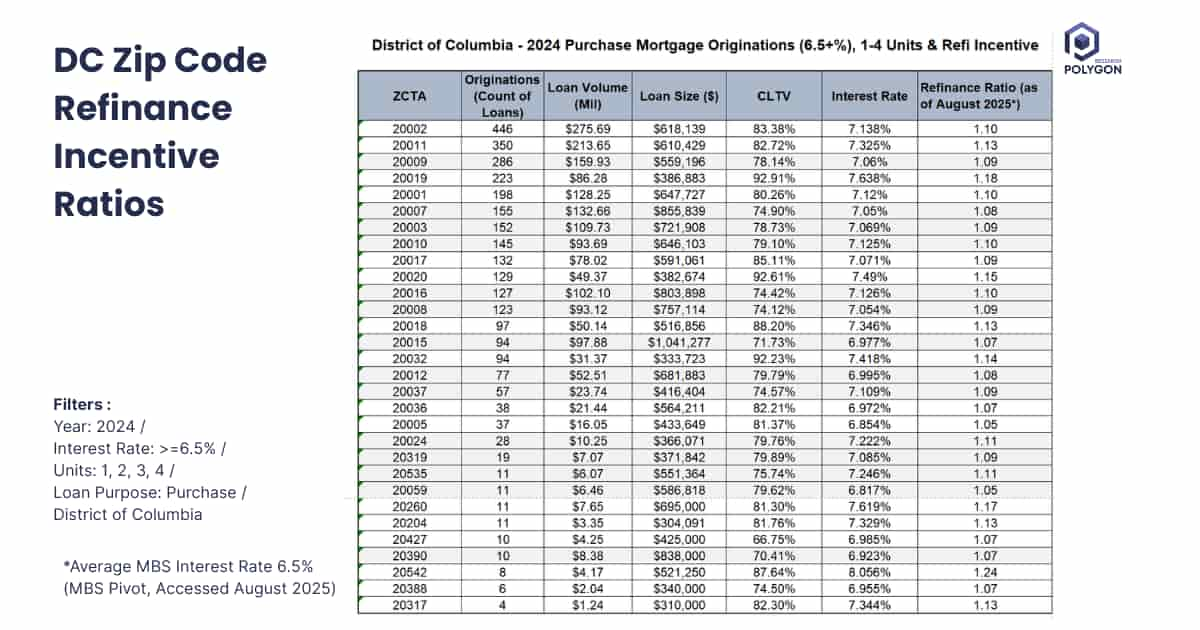

Mortgage lending is hyperlocal, varying significantly neighborhood to neighborhood. Using HMDA 2024 data (in HMDAVision) filtered for loans ≥6.5% vs. average (2025YTD) MBS rate of 6.5%, refinance incentive ratios across DC zip codes range from 1.05 to 1.24.

High-ratio areas like 20542 (1.24 ratio, 87.64% CLTV) show strong rate motivation but limited equity for traditional refinancing, requiring specialized high-LTV products.

Optimal strategy targets moderate-ratio, high-volume zones (20002: 1.10 ratio, 446 loans, 83.38% CLTV) where meaningful rate savings combine with adequate equity for streamlined approvals.

Low-ratio areas (20005, 20059) with sub-82% CLTVs represent premium borrowers ideal for relationship-based retention campaigns.

Lenders should stratify marketing by both incentive ratio and equity position, avoiding high-cost acquisition in equity-constrained markets while maximizing conversion in the sweet spot of motivated, qualified borrowers.

This hyperlocal intelligence enables precision marketing allocation, optimized territories, and data-driven advertising in the post-trigger-lead landscape.

From Analysis to Action

Ready to Continue? Get Your Exact Market Answers.

Start your 7-day free trial.