Latest Credit Union Delinquency Trends: Q2 2025

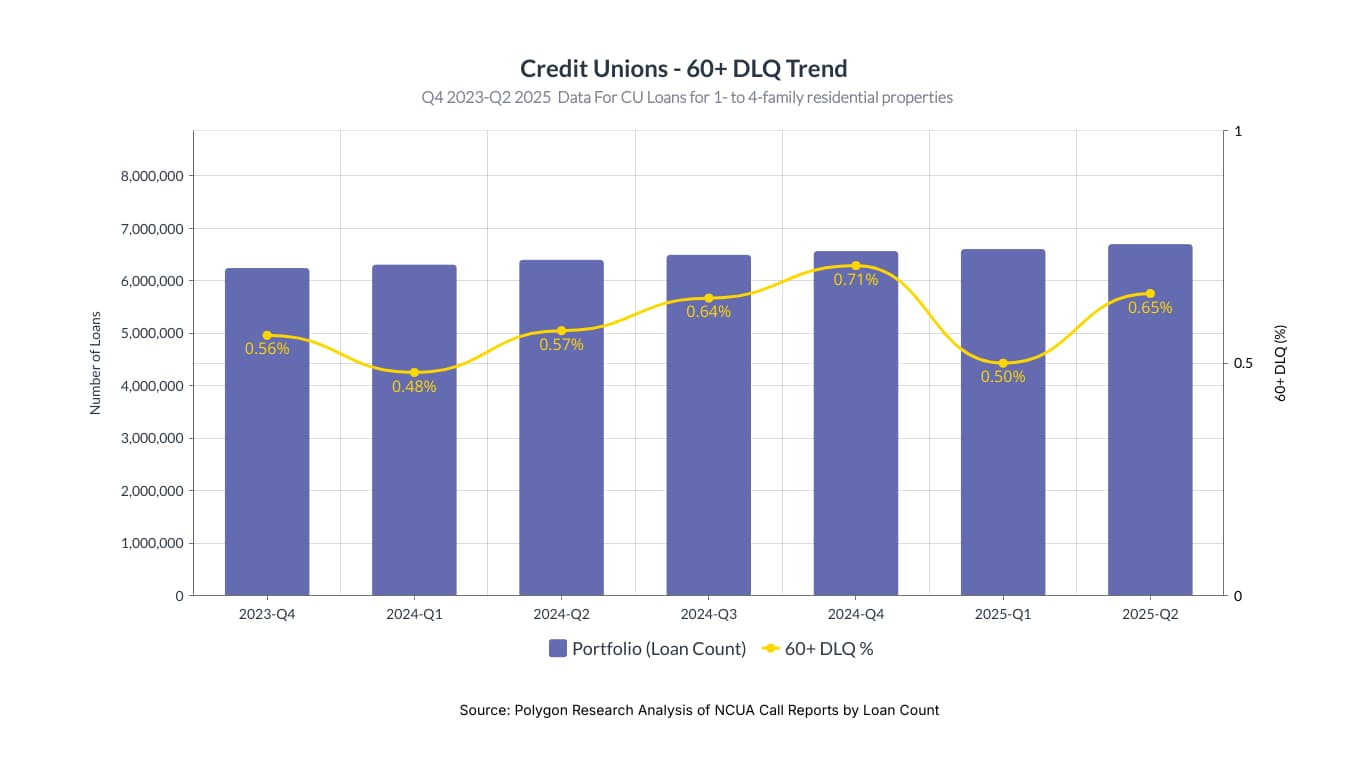

Credit union 60+ day delinquencies (by loan count) show a pattern of seasonal volatility, with year-end peaks and first-quarter troughs.

The spike in Q2 2025 continues this trend and signals a potential increase in portfolio credit risk and an early warning of growing financial stress among the member base.

Understanding this rhythm is helpful for proactive risk management. Credit union leaders can anticipate higher delinquencies toward year-end and adjust collections and loss mitigation strategies, for instance, by increasing member outreach in Q3 and Q4.

The Q2 2025 spike should prompt an immediate review of loan loss reserves and capital adequacy to ensure preparedness for a continued upward trend.

These insights also provide valuable macro-level context for re-evaluating underwriting standards and product features. By benchmarking their own performance against these national trends distilled from NCUA Call Reports, credit unions can better assess their relative risk exposure and the effectiveness of their member support strategies.

From Analysis to Action

Ready to Continue? Get Your Exact Market Answers.

Start your 7-day free trial.