Mortgage Borrower Age Trends vs. NAR Homebuyer Profile Insights

Recent narratives have painted a picture of a rapidly aging homebuyer, causing concern about the future of the housing industry. This chart, however, provides critical context for lenders, builders, and servicers by filtering for the true engine of the mortgage finance industry: Primary Residence Purchase Originations.

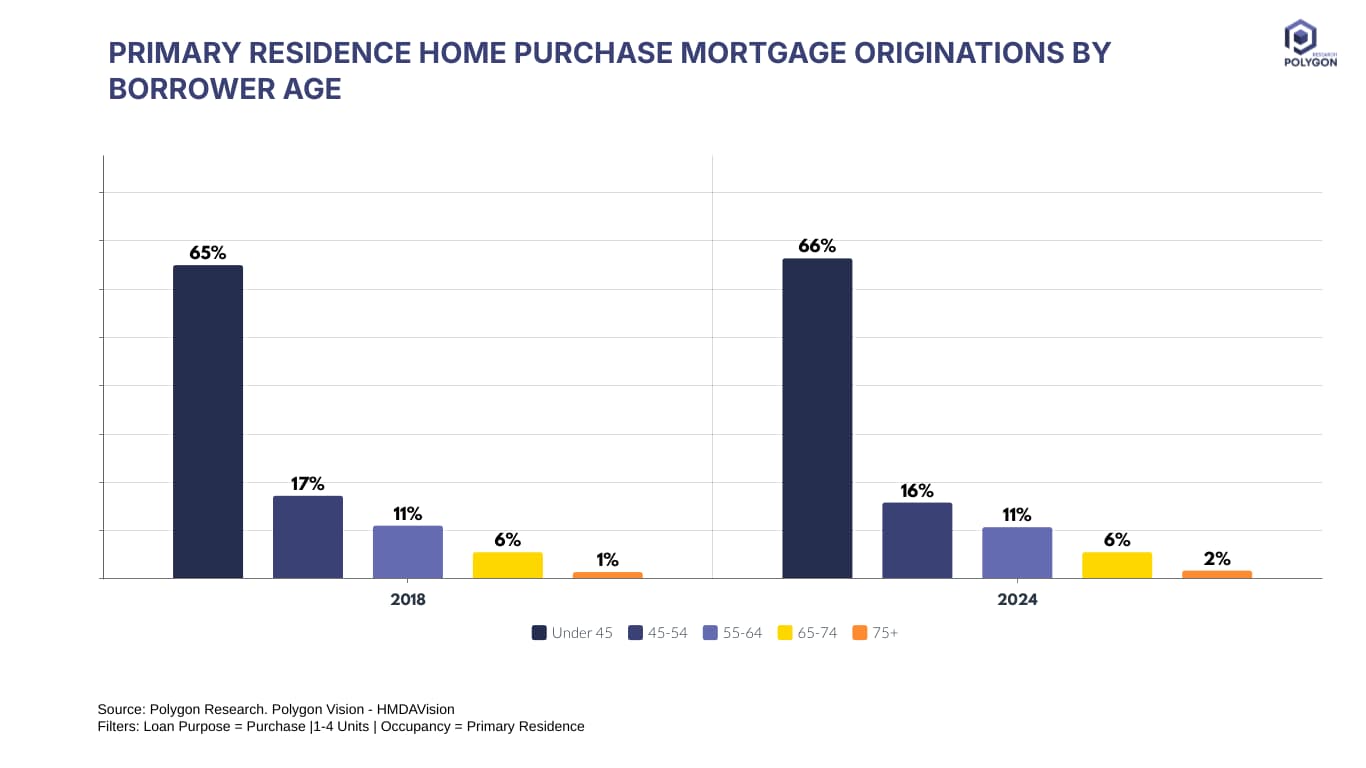

The data tells a starkly different and remarkably stable story. In 2024, a full 66% of all primary residence purchase mortgages were originated by borrowers under the age of 45. This is not an anomaly; it is virtually unchanged from 2018, when this same group accounted for 65% of the market. The 45-54 age bracket (16%) and 55-64 bracket (11%) hold significant, but decidedly secondary, market shares.

The mortgage-dependent homebuyer market remains anchored by younger borrowers, under the age of 45. What are the implications for various stakeholders?

Lenders: Do not misallocate resources by pivoting your entire strategy to an older buyer demographic. Your product development (e.g., FTHB programs, DPA solutions) and marketing outreach must remain intensely focused on the under-45 demographic.

Builders: The demand for entry-level homes, which requires mortgage financing, is not evaporating. This data confirms the structural demand from younger generations is stable and robust.

Policymakers: Efforts to improve mortgage affordability and access continue for this younger demographic, as they constitute the clear majority of the primary-residence mortgage market.

From Analysis to Action

Ready to Continue? Get Your Exact Market Answers.

Start your 7-day free trial.