Refinance Costs Analysis: Comparing Borrower-Paid Fees by Lender Type

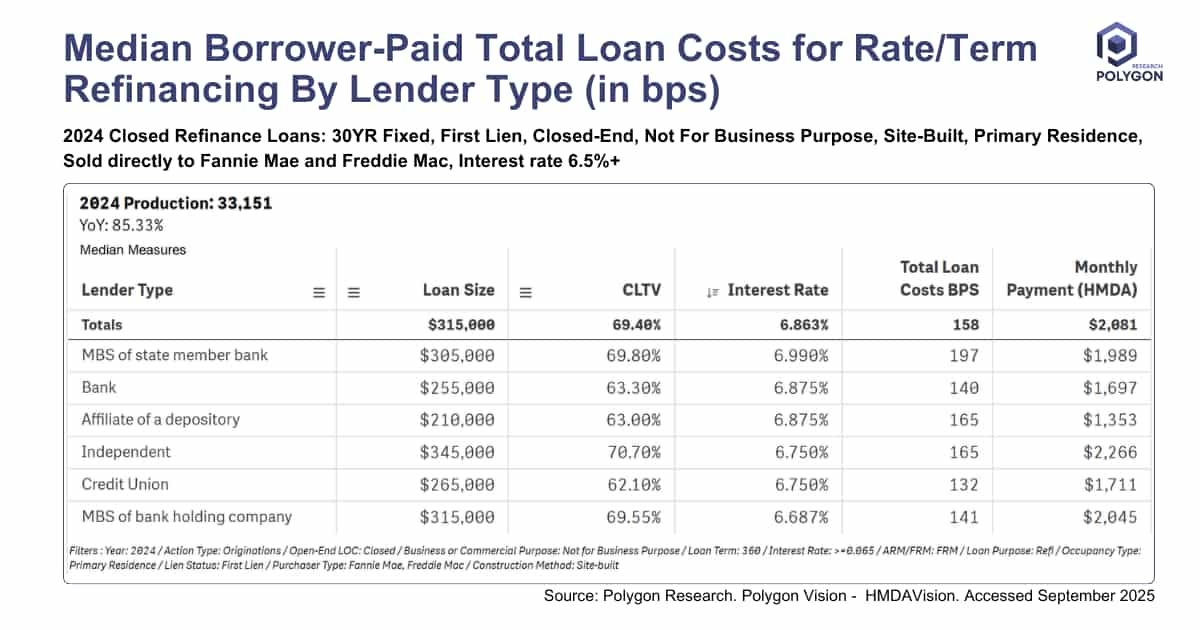

Clear lines emerged in the 2024 rate/term refi market for prime, GSE-eligible loans. Credit unions are the undisputed price leaders, charging a median of only 132 bps by serving a low-risk segment: borrowers with the most home equity (median CLTV of 62.10%).

IMBs are playing a different game, tackling larger loans ($345,000) for borrowers with less equity (CLTV of 70.70%), which is reflected in their higher costs (165 bps). Banks and depository affiliates land in the middle. While this national snapshot is a critical benchmark, the real competition is always local. HMDAVision users can instantly filter this analysis to their specific county or MSA to see exactly where they stand against their true competitors.

Credit Unions' low-cost leadership creates a retention paradox. Prime, high-equity members are the most attractive targets for competitors. The strategic imperative is to build loyalty beyond price - e.g. proactively offer HELOCs to deepen the member relationship before they are lured away.

Promptly diagnose your strategy. Are your higher fees intentional (a reflection of your risk appetite for higher-LTV) or a result of operational friction? Use these benchmarks to sharpen your efficiency or to double-down on a value proposition (e.g., speed, specialized products) that justifies your premium in your specific markets.

From Analysis to Action

Ready to Continue? Get Your Exact Market Answers.

Start your 7-day free trial.