Who Leads in ARM Cash-Out Refinancing? A 2024 HMDA Lender Ranking

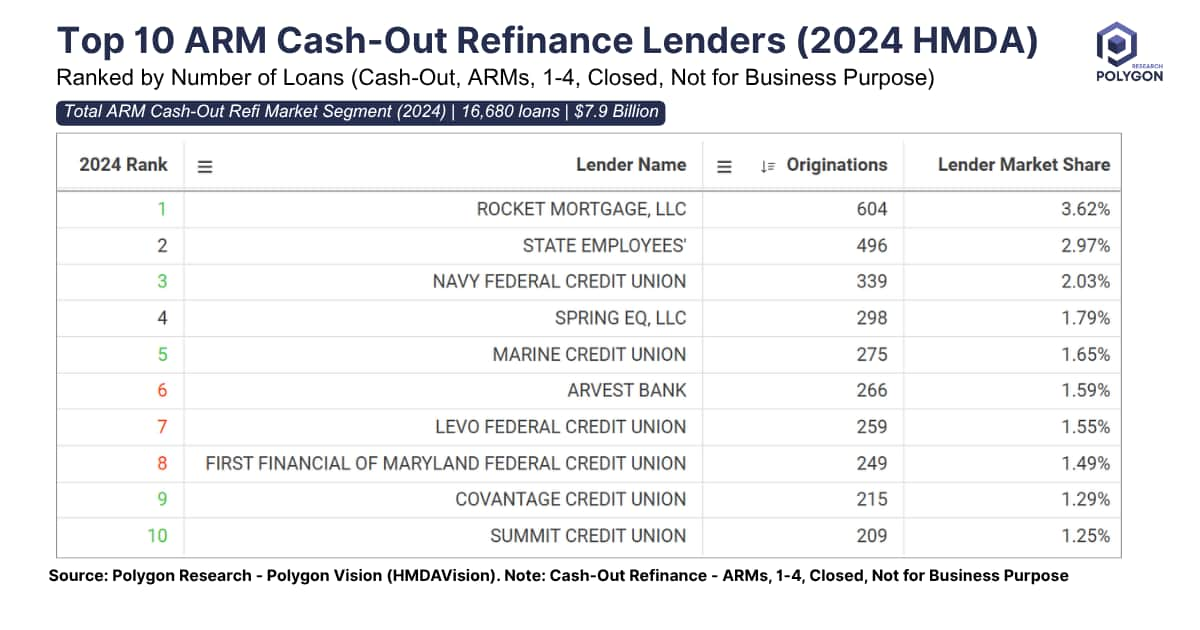

This chart, based on 2024 Home Mortgage Disclosure Act (HMDA) data, ranks the top 10 lenders for closed, 1-4 unit ARM cash-out refinances. The total market segment is substantial, comprising 16,680 loans valued at $7.9 billion.

Previously we focused on rate and term ARMs. It's helpful to look at refinances by these two segments because cash-out and rate-and-term refinances are driven by different economic factors and reflect distinct borrower motivations. Separating them allows lenders to better forecast volume, manage risk, and tailor their marketing and product strategies.

The leading lender, Rocket Mortgage, captured a 3.62% market share with 604 originations.

The most compelling takeaway is the dominance of credit unions. Institutions like State Employees', Navy Federal, and others occupy seven of the top ten spots. This success highlights a key strategic advantage: credit unions often leverage their member-centric model to excel in niche products.

Analyzing these two segments separately is crucial for forecasting and staffing, marketing and product strategy, and risk management. Cash-out refinances increase the borrower's total indebtedness and reduce their equity cushion, representing a potentially higher credit risk that must be managed and priced accordingly.

From Analysis to Action

Ready to Continue? Get Your Exact Market Answers.

Start your 7-day free trial.