Top First-Time Homebuyer Purchase Mortgage Markets by State, YTD 2026

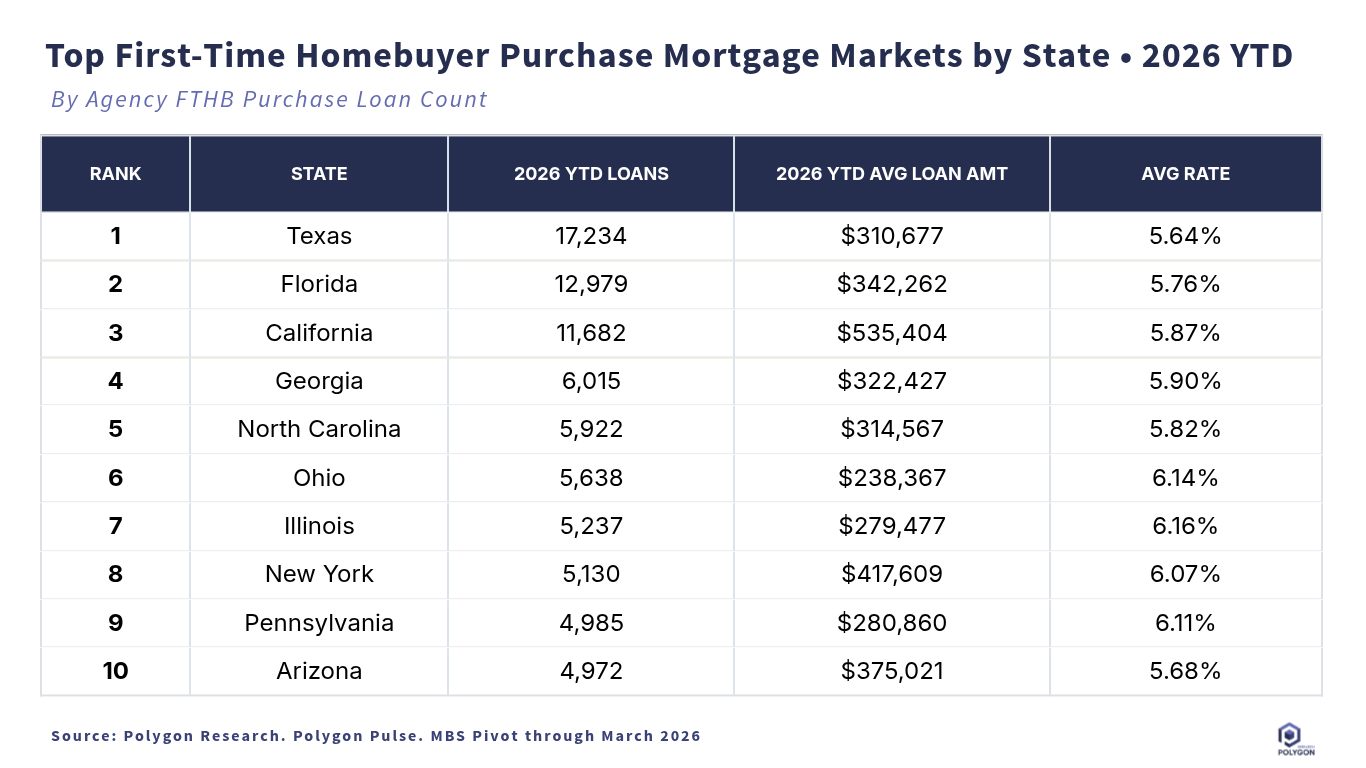

The top-10 states for YTD 2026 first-time homebuyer agency purchase originations show where entry-level demand is still converting into closed loans. Texas leads with 17,234 loans, followed by Florida at 12,979 and California at 11,682.

But the more useful insight is in the mix, not just the ranking. Texas combines the highest loan count with a below-average loan size and rate, suggesting a market where affordability and agency execution are still working at scale. California produces substantial volume, but with an average loan amount above $535,000, the borrower qualification challenge is very different. Ohio, Illinois, Pennsylvania, and New York show higher average rates than the total, which may reflect differences in product mix, credit profile, geography, or channel execution.

For lenders, this chart is a production strategy tool. High-volume states deserve capacity, referral partnerships, builder relationships, and localized pricing discipline. Higher-balance markets require tighter attention to income qualification, LLPAs, jumbo-conforming boundaries, and fallout risk. The point is not to chase volume blindly; it is to understand where first-time buyer demand is financeable, where margins are defendable, and where borrower education can turn affordability pressure into closed loans.

From Analysis to Action

Ready to Continue? Get Your Exact Market Answers.

Start your 7-day free trial.