Coming up with useful mortgage content can be difficult, especially when marketing is only one part of your job and mortgage marketing comes with real compliance concerns.

Loan officers, mortgage brokers, community bank and credit union teams are often told to post more, send more emails, and educate more borrowers. Then comes the hard part: What should we talk about?

HMDA data, benchmark reports, and your own production results can show what borrowers in your market are doing, where they are struggling, which loan products they use, and how their costs compare. Those findings can become practical content for borrowers, members, real estate partners, and employees.

Start with one useful local fact and answer a simple question:

What could someone learn from this?

Suppose your data shows that first-time homebuyers account for a growing share of purchases in your area.

A local first-time homebuyer trend can lead naturally to related topics such as down payment assistance, affordability, and the local homebuying market.

Perhaps your data shows that monthly housing costs are increasing faster than borrower incomes. That creates an opening to discuss mortgage affordability in a concrete way:

That finding could lead to content about how much home a buyer can afford, how interest rates affect the monthly payment, or which costs buyers should include in their budget.

The same process works with mortgage costs. Borrowers commonly compare interest rates while paying less attention to points, lender credits, origination charges, and other fees.

Local loan data may show meaningful differences in what borrowers pay. That finding can become an explanation of mortgage loan costs, discount points, APR, or how to compare loan offers.

The data gives you the reason to cover the topic. The article, video, or email should help the borrower understand it.

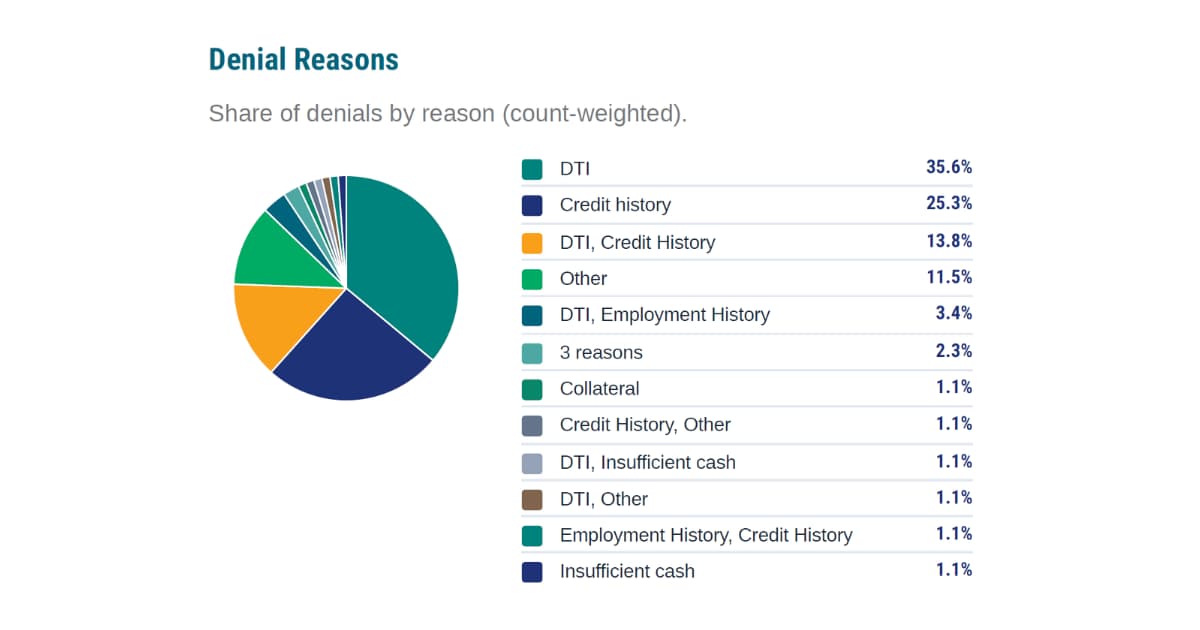

Mortgage application outcomes are another useful source of content ideas.

If debt-to-income ratio is a common denial reason in your market, create content explaining how lenders calculate it and what a prospective borrower can review before applying.

If credit history frequently affects applications, explain the role credit plays in mortgage approval.

If many applications remain incomplete or fail to reach closing, look more closely at your own process. Borrowers may need clearer instructions, earlier conversations, or a simple checklist of required documents.

Useful topics might include:

These subjects are highly relevant to borrowers and closely connected to the questions people ask search engines, AI assistants, loan officers, and housing counselors.

They also support better conversations inside the organization. A loan officer can use the same finding to explain why prospective buyers should begin preparing before they find a home.

Mortgage data can also reveal where your organization performs well.

A credit union may lead other credit unions in first-time homebuyer lending within a county. A community lender may have lower average origination charges than the broader market. A mortgage broker may have particular experience with a loan product that is growing locally.

Those findings can support strong marketing claims when the language is precise.

A broad statement such as “leading mortgage lender” tells the reader very little.

A more useful claim would be:

Ranked first by 2025 home-purchase loan count among credit unions in Smith County, based on HMDA data

Then add a source line that reflects how the analysis was completed:

For a Polygon Research Benchmark Report:

Source: Polygon Research analysis of 2025 HMDA data, ACUMA Benchmark Report.

For analysis completed by the lender in HMDAVision:

Source: Company X analysis of 2025 HMDA data using Polygon Research’s HMDAVision.

Include the year, geography, loan type, metric, and comparison group in the claim itself. Keep a record of the filters and selections used in HMDAVision so the analysis can be reproduced and reviewed.

That claim identifies the metric, year, geography, comparison group, and source.

The same principle applies to statements about borrower costs, market share, loan products, and customer groups. Include enough detail for someone to understand exactly what the number represents.

Keep a record of the source, filters, timeframe, and calculation behind every public claim. Claims about rates, fees, rankings, borrower outcomes, or demographic groups should go through your normal compliance or legal review.

Historical mortgage rates also need careful treatment. A rate reported in last year’s HMDA data describes a past loan. It should never appear to be an offer available today.

Some findings are better suited for internal use. Fair lending results, demographic gaps, and differences in application outcomes may point to important work involving outreach, products, employee training, partnerships, or the borrower experience. Review those findings internally before turning them into public messaging.

One useful finding can lead to several related pieces of content. A first-time homebuyer trend might become an article about preparing to buy, followed by content about affordability, down payment assistance, and the costs borrowers should compare when choosing a mortgage.

Together, those topics can help someone move from an initial question to a better understanding of the full homebuying process.

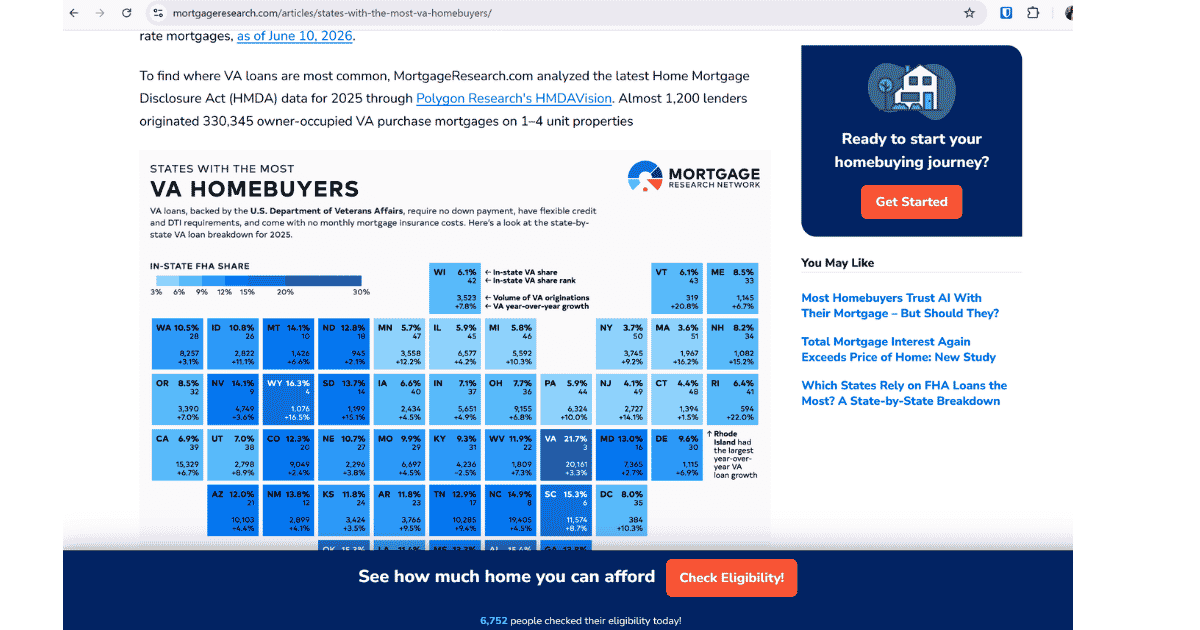

A good example comes from an HMDAVision user that publishes consumer-facing mortgage articles based on HMDA data. The article shown here uses state-level VA lending activity to answer a question homebuyers may search for, then connects the reader to calculators and eligibility tools.

This is where market data becomes more than a report. A useful data point can become searchable content, borrower education, and a clear path for the reader to take the next step.

This article is based on our webinar, Turn Local Mortgage Data into Homeownership Month Marketing Ideas.

Watch the replay to see examples of how local mortgage data can support borrower education, marketing content, loan officer conversations, and internal planning.

You can also learn more about the ACUMA Benchmark Report and how local HMDA data can help credit unions understand their market, compare performance, and find practical opportunities to serve members.

Learn how mortgage lenders, brokers, and credit unions can use local HMDA data to create useful content about first-time buyers, affordability, loan costs, and application barriers.

Coming up with useful mortgage content can be difficult, especially when marketing is only one part of your job and mortgage marketing comes with real compliance concerns.

Loan officers, mortgage brokers, community bank and credit union teams are often told to post more, send more emails, and educate more borrowers. Then comes the hard part: What should we talk about?

HMDA data, benchmark reports, and your own production results can show what borrowers in your market are doing, where they are struggling, which loan products they use, and how their costs compare. Those findings can become practical content for borrowers, members, real estate partners, and employees.

Start with one useful local fact and answer a simple question:

What could someone learn from this?

Suppose your data shows that first-time homebuyers account for a growing share of purchases in your area.

A local first-time homebuyer trend can lead naturally to related topics such as down payment assistance, affordability, and the local homebuying market.

Perhaps your data shows that monthly housing costs are increasing faster than borrower incomes. That creates an opening to discuss mortgage affordability in a concrete way:

That finding could lead to content about how much home a buyer can afford, how interest rates affect the monthly payment, or which costs buyers should include in their budget.

The same process works with mortgage costs. Borrowers commonly compare interest rates while paying less attention to points, lender credits, origination charges, and other fees.

Local loan data may show meaningful differences in what borrowers pay. That finding can become an explanation of mortgage loan costs, discount points, APR, or how to compare loan offers.

The data gives you the reason to cover the topic. The article, video, or email should help the borrower understand it.

Mortgage application outcomes are another useful source of content ideas.

If debt-to-income ratio is a common denial reason in your market, create content explaining how lenders calculate it and what a prospective borrower can review before applying.

If credit history frequently affects applications, explain the role credit plays in mortgage approval.

If many applications remain incomplete or fail to reach closing, look more closely at your own process. Borrowers may need clearer instructions, earlier conversations, or a simple checklist of required documents.

Useful topics might include:

These subjects are highly relevant to borrowers and closely connected to the questions people ask search engines, AI assistants, loan officers, and housing counselors.

They also support better conversations inside the organization. A loan officer can use the same finding to explain why prospective buyers should begin preparing before they find a home.

Mortgage data can also reveal where your organization performs well.

A credit union may lead other credit unions in first-time homebuyer lending within a county. A community lender may have lower average origination charges than the broader market. A mortgage broker may have particular experience with a loan product that is growing locally.

Those findings can support strong marketing claims when the language is precise.

A broad statement such as “leading mortgage lender” tells the reader very little.

A more useful claim would be:

Ranked first by 2025 home-purchase loan count among credit unions in Smith County, based on HMDA data

Then add a source line that reflects how the analysis was completed:

For a Polygon Research Benchmark Report:

Source: Polygon Research analysis of 2025 HMDA data, ACUMA Benchmark Report.

For analysis completed by the lender in HMDAVision:

Source: Company X analysis of 2025 HMDA data using Polygon Research’s HMDAVision.

Include the year, geography, loan type, metric, and comparison group in the claim itself. Keep a record of the filters and selections used in HMDAVision so the analysis can be reproduced and reviewed.

That claim identifies the metric, year, geography, comparison group, and source.

The same principle applies to statements about borrower costs, market share, loan products, and customer groups. Include enough detail for someone to understand exactly what the number represents.

Keep a record of the source, filters, timeframe, and calculation behind every public claim. Claims about rates, fees, rankings, borrower outcomes, or demographic groups should go through your normal compliance or legal review.

Historical mortgage rates also need careful treatment. A rate reported in last year’s HMDA data describes a past loan. It should never appear to be an offer available today.

Some findings are better suited for internal use. Fair lending results, demographic gaps, and differences in application outcomes may point to important work involving outreach, products, employee training, partnerships, or the borrower experience. Review those findings internally before turning them into public messaging.

One useful finding can lead to several related pieces of content. A first-time homebuyer trend might become an article about preparing to buy, followed by content about affordability, down payment assistance, and the costs borrowers should compare when choosing a mortgage.

Together, those topics can help someone move from an initial question to a better understanding of the full homebuying process.

A good example comes from an HMDAVision user that publishes consumer-facing mortgage articles based on HMDA data. The article shown here uses state-level VA lending activity to answer a question homebuyers may search for, then connects the reader to calculators and eligibility tools.

This is where market data becomes more than a report. A useful data point can become searchable content, borrower education, and a clear path for the reader to take the next step.

This article is based on our webinar, Turn Local Mortgage Data into Homeownership Month Marketing Ideas.

Watch the replay to see examples of how local mortgage data can support borrower education, marketing content, loan officer conversations, and internal planning.

You can also learn more about the ACUMA Benchmark Report and how local HMDA data can help credit unions understand their market, compare performance, and find practical opportunities to serve members.

Yes, some findings can support public content, especially rank, market share, category leadership, and comparative cost findings. The claim should include the metric, geography, year, and source, and the finished piece should go through your normal compliance review.

You may be able to, but it usually creates more risk and distraction than value. An aggregate market comparison is often cleaner: compared with all other lenders in the county, or compared with the county market average. Your compliance team should review any claim involving a named competitor.

The Benchmark Report is a prepared snapshot of the lender’s performance and market position. HMDAVision is the interactive analysis environment. It allows you to change markets, borrower segments, products, competitors, and other filters and continue investigating beyond the report.

HMDAVision allows smaller credit unions and community banks to study the lenders, borrowers, products, and neighborhoods in the markets they serve. They can use that information to understand competitors, identify first-time homebuyer and affordability opportunities, support fair lending analysis, evaluate branch and loan officer placement, and develop useful talking points and educational content for members.