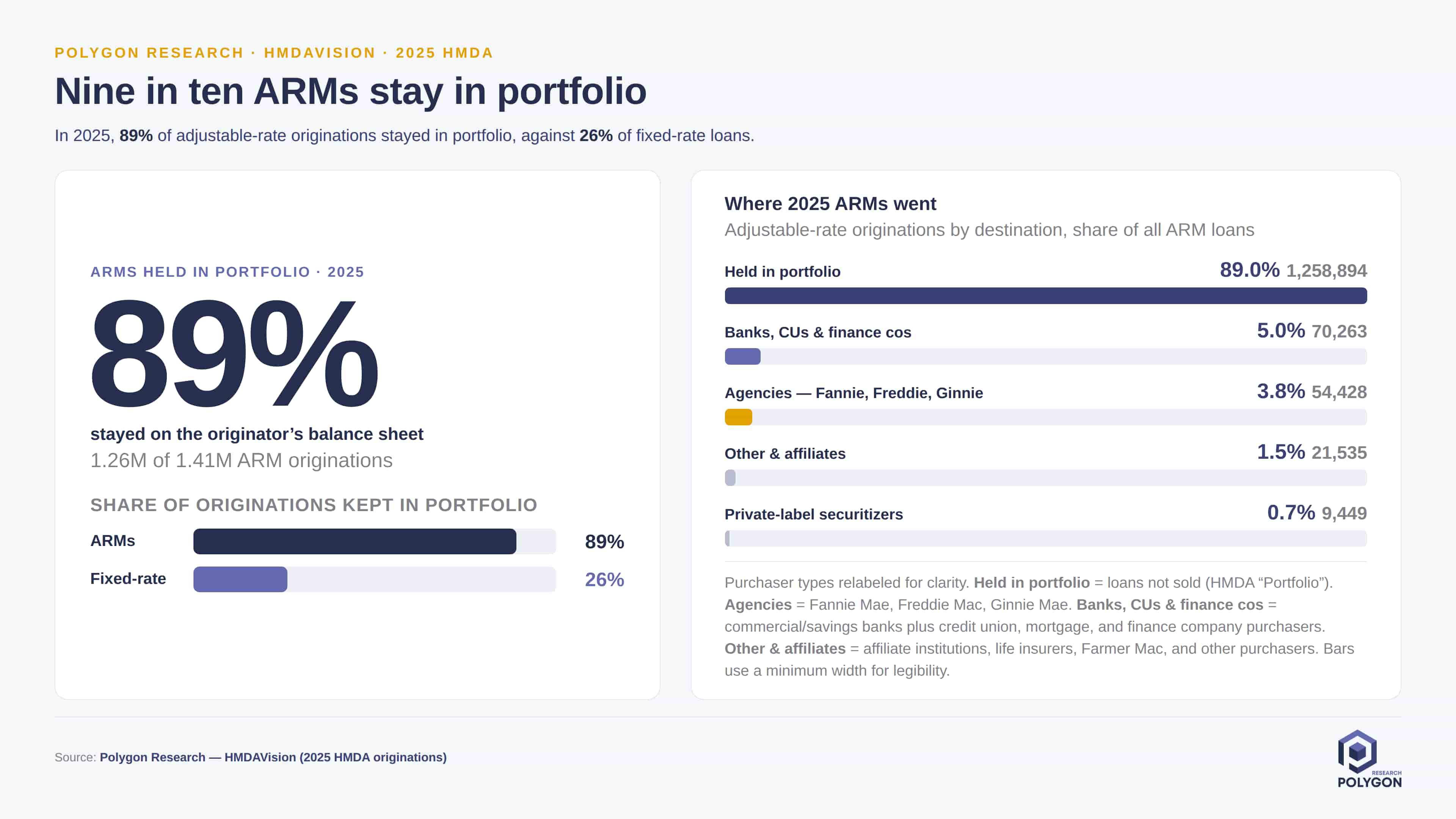

Adjustable-Rate Mortgages Held in Portfolio

Among the 2025 HMDA originations shown, 89.0% of ARMs—1,258,894 loans—were reported as “Portfolio,” meaning the loans were not sold. By comparison, 26% of fixed-rate originations were held in portfolio.

Reported sales were dispersed across several purchaser groups. Banks, credit unions and finance companies acquired 5.0% of ARMs, or 70,263 loans. Fannie Mae, Freddie Mac and Ginnie Mae accounted for 3.8%, or 54,428 loans. Other purchasers and affiliates represented 1.5%, and private-label securitizers 0.7%.

For depositories, the 89% portfolio share provides a benchmark for ARM balance-sheet appetite, concentration and liquidity capacity. Polygon’s Agency ARM share, Agency ARM lender rankings and Agency ARM borrower credit profile provide broader context for the agency segment. Together, these views show how agency activity is changing, which seller/issuers are most active and how the borrower credit mix has shifted since 2021. Product, capital-markets and risk teams can use the combined picture to evaluate portfolio retention, agency eligibility and execution, pricing, funding capacity and layered-risk exposure.

HMDA purchaser type identifies whether and to whom a loan was sold; it does not explain why a loan was retained, whether it was sold later, or the economics of the execution. Purchaser groups were relabeled for clarity.

From Analysis to Action

Ready to Continue? Get Your Exact Market Answers.

Start your 7-day free trial.