Agency adjustable-rate mortgages are returning to relevance in a mortgage market defined by elevated rates, high home prices, and persistent affordability pressure — and the borrowers and institutions driving that comeback look very different from those in the 2021 market.

Data source: Polygon Research, Polygon Pulse (MBS Pivot). The analysis covers agency loans represented in Fannie Mae, Freddie Mac and Ginnie Mae mortgage-backed securities data. Seller/issuer rankings are based on ARM loan count. YTD 2026 data is through May 2026.

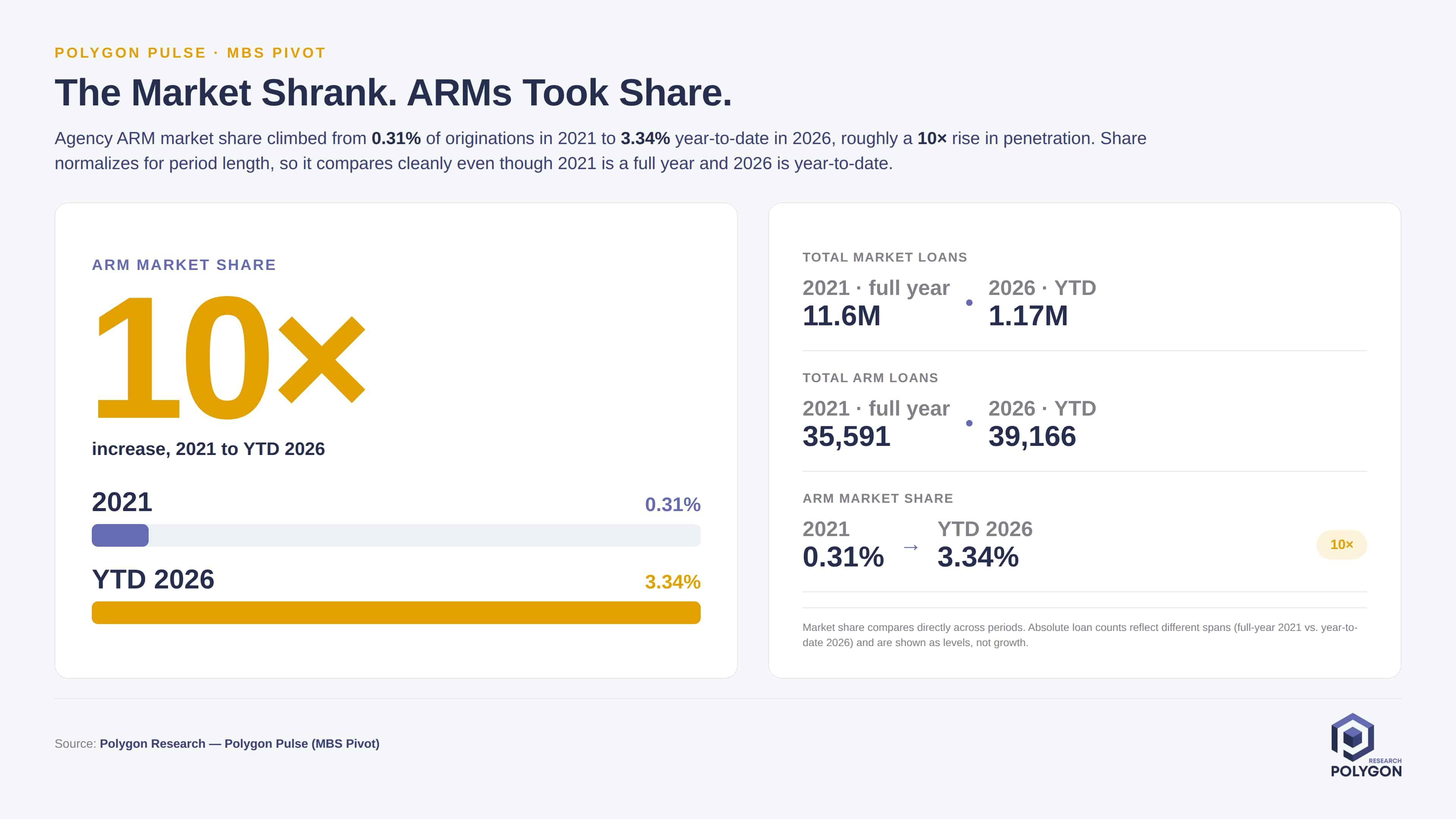

Agency ARMs accounted for just 0.31% of agency mortgage loans in 2021. By YTD 2026, their share had climbed to 3.34% — a tenfold increase that is especially notable given how different today's mortgage environment is from the low-rate market of five years ago. Borrowers now face a combination of higher monthly payments and home prices that remain elevated in most major markets, and an adjustable-rate mortgage's lower initial rate can help on both fronts: it can improve qualification, reduce the early payment burden, or allow a borrower to preserve more monthly cash flow.

ARMs remain a minority of total agency originations. What has changed is their role within the agency product mix — and the profile of the borrowers and lenders involved. ARM usage also varies considerably by geography; our earlier state-level adjustable-rate mortgage analysis found greater ARM penetration in several expensive housing markets where the difference between fixed and adjustable rates can have a larger effect on the monthly payment.

Download the Agency ARMs Market Share Chart.

The renewed use of adjustable-rate mortgages brings back a debate that predates the housing crisis. In February 2004, Federal Reserve Chairman Alan Greenspan argued that many homeowners could have saved tens of thousands of dollars by choosing ARMs over fixed-rate loans in the preceding decade. His reasoning was direct: a 30-year fixed-rate borrower pays a premium for long-term payment certainty and protection from rising rates. Borrowers with the capacity to manage interest-rate risk could potentially avoid that cost by accepting some variability in their payment.

Greenspan also acknowledged the limit of his own argument — those savings would have looked very different if rates had moved sharply higher. By July 2005, his tone had grown more cautious: he identified the rising prevalence of interest-only loans and more exotic ARM structures as a particular concern, even while allowing that adjustable-rate products could have appropriate uses for certain borrowers. That progression captures the central tension around ARMs. A lower initial rate can genuinely help a borrower manage the cost of purchasing a home. How much risk accompanies that benefit depends on the borrower's leverage, debt load, the structure of the loan, and the cushion available to absorb a future payment increase.

One structural feature of ARM pricing compounds that tension: the rate that gets quoted — by lenders, by the media, and in most borrower comparisons — is always the initial rate, regardless of how short the fixed period actually is. A 1/1 ARM and a 7/1 ARM may be quoted at similar rates, but their risk profiles for a borrower planning to stay ten years are entirely different. When affordability pressure is the primary driver of product selection, as the 2026 borrower data suggests it is, that gap between the quoted rate and the true cost of the loan over time deserves particular attention.

In 2021, five depository institutions appeared among the 10 largest agency ARM seller/issuers: Wells Fargo Bank, JPMorgan Chase Bank, Truist Bank, Citizens Bank, and U.S. Bank. Wells Fargo led the market with 6,013 loans. By YTD 2026, no depository institution remained in the top 10 — every position is now held by an independent mortgage bank or other non-depository lender.

The leading agency ARM seller/issuers in YTD 2026 are:

Download the Agency ARM Lender Rankings Chart.

The shift reflects a broader change in how agency mortgage production is organized. Many IMBs operate across retail, wholesale, and correspondent channels simultaneously, which allows them to introduce products quickly, reach a broad set of loan officers and brokers, and scale volume when borrower demand moves toward a particular product. For banks and credit unions, the rankings are a competitive signal worth taking seriously: ARM demand has not disappeared — it has shifted, largely toward nonbank lenders that have made the product a meaningful part of their affordability strategy.

Download the Agency ARM Borrower Credit Profile

The shift in lender leadership is significant. The shift in the borrower profile may be more consequential. Across four core credit measures, the YTD 2026 agency ARM borrower enters the market with less financial cushion than the 2021 borrower — and the changes are not marginal.

The average FICO score fell 29 points, from 766 to 737. An average of 737 still reflects a generally creditworthy borrower, but the decline shows that agency ARM usage has expanded well beyond the exceptionally high-credit population that dominated in 2021. At the same time, average LTV rose from 64% to 79%, meaning the typical borrower entered 2021 with roughly 36% equity and now enters with roughly 21%. These two trends together — modestly weaker credit and meaningfully lower equity — describe a borrower who has less room to absorb an adverse event before the loan becomes stressed.

Average DTI rose 8.2 percentage points, from 32.2% to 40.4%. That increase indicates that current ARM borrowers are committing a substantially larger share of monthly income to debt service — which supports the view that the initial payment savings are not incidental to the decision. For a meaningful share of these borrowers, the ARM's lower introductory rate is likely what makes the purchase work financially, either for qualification, monthly cash flow, or both.

The most striking shift involves borrowers at the top of the LTV range. In 2021, just 0.4% of agency ARMs carried LTV ratios between 97% and 100%. In YTD 2026, that share is 15.7% — roughly 39 times higher. High LTV alone does not determine whether a loan will perform, but when it appears alongside higher DTI and the possibility of a future rate adjustment, it concentrates the risk profile in a way that warrants closer attention as these loans season.

Three connected forces explain the trend. The most direct is affordability pressure: elevated rates and home prices have made the monthly cost of homeownership materially higher than it was in 2021, and an ARM's lower initial rate addresses that problem directly, whether by improving qualification, reducing the early payment, or both. For some borrowers, the calculus also rests on an expectation of refinancing, selling, or income growth before the first rate adjustment — outcomes that are plausible but not guaranteed.

The second force is IMB distribution capacity. Independent mortgage banks have not just responded to ARM demand — they have helped create it. Their presence across multiple origination channels gives them the ability to introduce products quickly, reach a broad range of loan officers and brokers, and price competitively as borrower interest builds. The third force is a structural expansion of the ARM borrower population itself. The movement in FICO, LTV, and DTI shows that ARMs are no longer concentrated among highly creditworthy, low-leverage borrowers. They are increasingly serving a segment of the market where affordability, qualification, and near-term cash flow carry greater weight in the product decision.

Today’s agency ARM market should not be equated with the full range of nontraditional mortgage products offered before the financial crisis.

The loans covered in this analysis entered agency or government mortgage-backed securities. They are distinct from the private-label option ARMs, negative-amortization products and loosely underwritten loans frequently associated with the pre-crisis market.

Product structure still matters.

ARM borrowers and loan officers should understand:

The current credit profile adds another layer to that evaluation. Compared with 2021, today’s agency ARM borrowers have higher leverage, greater debt burdens and less equity protection.

Averages provide a useful starting point, but the concentration of loans across multiple risk characteristics — high LTV, high DTI, lower FICO, in the same pool — reveals more than any single measure. Lenders should examine ARM production across FICO, LTV, DTI, geography, loan purpose, occupancy, and channel to understand where the population is clustering, not just where it centers.

A borrower choosing an ARM primarily to solve an immediate affordability problem needs a clear picture of what happens after the introductory period. That means a direct conversation about the adjustment schedule, the index, the lender's margin, rate caps, and the maximum possible payment — not just the initial rate. The affordability problem that brought the borrower to an ARM does not disappear at the first adjustment date. A disclosure checklist is not the same as a borrower who understands their exposure: research on ARM disclosure has long found that comprehensive feature lists tend to obscure the terms that matter most, and that overwhelming borrowers with information they cannot act on is functionally close to disclosing nothing at all.

Banks and credit unions should examine why IMBs now hold every top-10 agency ARM position. The relevant questions are specific: which lenders are gaining ARM production, which channels are driving volume, where the loans are concentrating geographically, and how ARM pricing compares with fixed-rate alternatives in their markets. The absence of depositories from the rankings is itself a data point that deserves a competitive response.

The charts in this analysis describe origination characteristics, not performance. The shift toward lower FICO, higher LTV, and higher DTI is an early credit-profile signal. Whether that movement translates into different delinquency, prepayment, or default outcomes will become clearer as the 2025 and 2026 cohorts age. Lenders with meaningful ARM exposure should be building the monitoring infrastructure now rather than waiting for early indicators to surface.

The agency ARM market has entered a different phase. Share has increased tenfold since 2021, IMBs have displaced depositories at the top of the rankings, and the average borrower now carries lower credit scores, more leverage, and a higher debt load. None of that makes ARMs unsuitable for the borrowers using them — it makes the underwriting, product design, borrower education, and performance monitoring more important. The agency ARM comeback deserves attention not just because of how much volume has grown, but because of who is leading it and who is borrowing.

Note: The data, research, and analysis are Polygon Research's own. AI tools were used to assist with writing and chart design.

Agency ARM share rose from 0.31% in 2021 to 3.34% YTD 2026. See which lenders lead and how borrower FICO, LTV and DTI have shifted.

Agency adjustable-rate mortgages are returning to relevance in a mortgage market defined by elevated rates, high home prices, and persistent affordability pressure — and the borrowers and institutions driving that comeback look very different from those in the 2021 market.

Data source: Polygon Research, Polygon Pulse (MBS Pivot). The analysis covers agency loans represented in Fannie Mae, Freddie Mac and Ginnie Mae mortgage-backed securities data. Seller/issuer rankings are based on ARM loan count. YTD 2026 data is through May 2026.

Agency ARMs accounted for just 0.31% of agency mortgage loans in 2021. By YTD 2026, their share had climbed to 3.34% — a tenfold increase that is especially notable given how different today's mortgage environment is from the low-rate market of five years ago. Borrowers now face a combination of higher monthly payments and home prices that remain elevated in most major markets, and an adjustable-rate mortgage's lower initial rate can help on both fronts: it can improve qualification, reduce the early payment burden, or allow a borrower to preserve more monthly cash flow.

ARMs remain a minority of total agency originations. What has changed is their role within the agency product mix — and the profile of the borrowers and lenders involved. ARM usage also varies considerably by geography; our earlier state-level adjustable-rate mortgage analysis found greater ARM penetration in several expensive housing markets where the difference between fixed and adjustable rates can have a larger effect on the monthly payment.

Download the Agency ARMs Market Share Chart.

The renewed use of adjustable-rate mortgages brings back a debate that predates the housing crisis. In February 2004, Federal Reserve Chairman Alan Greenspan argued that many homeowners could have saved tens of thousands of dollars by choosing ARMs over fixed-rate loans in the preceding decade. His reasoning was direct: a 30-year fixed-rate borrower pays a premium for long-term payment certainty and protection from rising rates. Borrowers with the capacity to manage interest-rate risk could potentially avoid that cost by accepting some variability in their payment.

Greenspan also acknowledged the limit of his own argument — those savings would have looked very different if rates had moved sharply higher. By July 2005, his tone had grown more cautious: he identified the rising prevalence of interest-only loans and more exotic ARM structures as a particular concern, even while allowing that adjustable-rate products could have appropriate uses for certain borrowers. That progression captures the central tension around ARMs. A lower initial rate can genuinely help a borrower manage the cost of purchasing a home. How much risk accompanies that benefit depends on the borrower's leverage, debt load, the structure of the loan, and the cushion available to absorb a future payment increase.

One structural feature of ARM pricing compounds that tension: the rate that gets quoted — by lenders, by the media, and in most borrower comparisons — is always the initial rate, regardless of how short the fixed period actually is. A 1/1 ARM and a 7/1 ARM may be quoted at similar rates, but their risk profiles for a borrower planning to stay ten years are entirely different. When affordability pressure is the primary driver of product selection, as the 2026 borrower data suggests it is, that gap between the quoted rate and the true cost of the loan over time deserves particular attention.

In 2021, five depository institutions appeared among the 10 largest agency ARM seller/issuers: Wells Fargo Bank, JPMorgan Chase Bank, Truist Bank, Citizens Bank, and U.S. Bank. Wells Fargo led the market with 6,013 loans. By YTD 2026, no depository institution remained in the top 10 — every position is now held by an independent mortgage bank or other non-depository lender.

The leading agency ARM seller/issuers in YTD 2026 are:

Download the Agency ARM Lender Rankings Chart.

The shift reflects a broader change in how agency mortgage production is organized. Many IMBs operate across retail, wholesale, and correspondent channels simultaneously, which allows them to introduce products quickly, reach a broad set of loan officers and brokers, and scale volume when borrower demand moves toward a particular product. For banks and credit unions, the rankings are a competitive signal worth taking seriously: ARM demand has not disappeared — it has shifted, largely toward nonbank lenders that have made the product a meaningful part of their affordability strategy.

Download the Agency ARM Borrower Credit Profile

The shift in lender leadership is significant. The shift in the borrower profile may be more consequential. Across four core credit measures, the YTD 2026 agency ARM borrower enters the market with less financial cushion than the 2021 borrower — and the changes are not marginal.

The average FICO score fell 29 points, from 766 to 737. An average of 737 still reflects a generally creditworthy borrower, but the decline shows that agency ARM usage has expanded well beyond the exceptionally high-credit population that dominated in 2021. At the same time, average LTV rose from 64% to 79%, meaning the typical borrower entered 2021 with roughly 36% equity and now enters with roughly 21%. These two trends together — modestly weaker credit and meaningfully lower equity — describe a borrower who has less room to absorb an adverse event before the loan becomes stressed.

Average DTI rose 8.2 percentage points, from 32.2% to 40.4%. That increase indicates that current ARM borrowers are committing a substantially larger share of monthly income to debt service — which supports the view that the initial payment savings are not incidental to the decision. For a meaningful share of these borrowers, the ARM's lower introductory rate is likely what makes the purchase work financially, either for qualification, monthly cash flow, or both.

The most striking shift involves borrowers at the top of the LTV range. In 2021, just 0.4% of agency ARMs carried LTV ratios between 97% and 100%. In YTD 2026, that share is 15.7% — roughly 39 times higher. High LTV alone does not determine whether a loan will perform, but when it appears alongside higher DTI and the possibility of a future rate adjustment, it concentrates the risk profile in a way that warrants closer attention as these loans season.

Three connected forces explain the trend. The most direct is affordability pressure: elevated rates and home prices have made the monthly cost of homeownership materially higher than it was in 2021, and an ARM's lower initial rate addresses that problem directly, whether by improving qualification, reducing the early payment, or both. For some borrowers, the calculus also rests on an expectation of refinancing, selling, or income growth before the first rate adjustment — outcomes that are plausible but not guaranteed.

The second force is IMB distribution capacity. Independent mortgage banks have not just responded to ARM demand — they have helped create it. Their presence across multiple origination channels gives them the ability to introduce products quickly, reach a broad range of loan officers and brokers, and price competitively as borrower interest builds. The third force is a structural expansion of the ARM borrower population itself. The movement in FICO, LTV, and DTI shows that ARMs are no longer concentrated among highly creditworthy, low-leverage borrowers. They are increasingly serving a segment of the market where affordability, qualification, and near-term cash flow carry greater weight in the product decision.

Today’s agency ARM market should not be equated with the full range of nontraditional mortgage products offered before the financial crisis.

The loans covered in this analysis entered agency or government mortgage-backed securities. They are distinct from the private-label option ARMs, negative-amortization products and loosely underwritten loans frequently associated with the pre-crisis market.

Product structure still matters.

ARM borrowers and loan officers should understand:

The current credit profile adds another layer to that evaluation. Compared with 2021, today’s agency ARM borrowers have higher leverage, greater debt burdens and less equity protection.

Averages provide a useful starting point, but the concentration of loans across multiple risk characteristics — high LTV, high DTI, lower FICO, in the same pool — reveals more than any single measure. Lenders should examine ARM production across FICO, LTV, DTI, geography, loan purpose, occupancy, and channel to understand where the population is clustering, not just where it centers.

A borrower choosing an ARM primarily to solve an immediate affordability problem needs a clear picture of what happens after the introductory period. That means a direct conversation about the adjustment schedule, the index, the lender's margin, rate caps, and the maximum possible payment — not just the initial rate. The affordability problem that brought the borrower to an ARM does not disappear at the first adjustment date. A disclosure checklist is not the same as a borrower who understands their exposure: research on ARM disclosure has long found that comprehensive feature lists tend to obscure the terms that matter most, and that overwhelming borrowers with information they cannot act on is functionally close to disclosing nothing at all.

Banks and credit unions should examine why IMBs now hold every top-10 agency ARM position. The relevant questions are specific: which lenders are gaining ARM production, which channels are driving volume, where the loans are concentrating geographically, and how ARM pricing compares with fixed-rate alternatives in their markets. The absence of depositories from the rankings is itself a data point that deserves a competitive response.

The charts in this analysis describe origination characteristics, not performance. The shift toward lower FICO, higher LTV, and higher DTI is an early credit-profile signal. Whether that movement translates into different delinquency, prepayment, or default outcomes will become clearer as the 2025 and 2026 cohorts age. Lenders with meaningful ARM exposure should be building the monitoring infrastructure now rather than waiting for early indicators to surface.

The agency ARM market has entered a different phase. Share has increased tenfold since 2021, IMBs have displaced depositories at the top of the rankings, and the average borrower now carries lower credit scores, more leverage, and a higher debt load. None of that makes ARMs unsuitable for the borrowers using them — it makes the underwriting, product design, borrower education, and performance monitoring more important. The agency ARM comeback deserves attention not just because of how much volume has grown, but because of who is leading it and who is borrowing.

Note: The data, research, and analysis are Polygon Research's own. AI tools were used to assist with writing and chart design.

Yes. Agency ARM market share increased from 0.31% in 2021 to 3.34% YTD 2026. That represents an increase of ten times, although ARMs still account for a minority of total agency mortgage originations.

PennyMac Loan Services ranked first among agency ARM seller/issuers in YTD 2026, with 4,675 loans during the period analyzed.

Today’s agency ARM market differs from the private-label option ARMs and other exotic mortgage products associated with the pre-crisis period. The loans analyzed here entered Fannie Mae, Freddie Mac or Ginnie Mae securities. Borrower leverage, DTI, product terms and future payment exposure still require careful evaluation.

MBS Pivot allows mortgage professionals to examine agency ARM activity by seller/issuer, geography, agency, channel, loan purpose, FICO, LTV, DTI and other loan characteristics.